In today's financial landscape, understanding the balance transfer card limit is essential for managing your credit effectively. As individuals increasingly seek ways to consolidate debt and reduce interest payments, balance transfer cards have gained immense popularity. These cards allow you to transfer high-interest credit card debt to a new card with a lower interest rate, providing a strategic advantage for financial management.

This article will dive deep into the intricate details surrounding balance transfer cards, including how they work, the factors that influence your credit limit, and tips for maximizing their benefits. By the end of this comprehensive guide, you will have a clearer understanding of balance transfer cards and their limits, empowering you to make informed financial decisions.

Whether you're looking to pay off existing debt or simply want to take advantage of lower interest rates, knowing how balance transfer card limits work is crucial for achieving your financial goals. Let’s explore the fundamentals of balance transfer cards and how to navigate their limits effectively.

Table of Contents

- What is a Balance Transfer Card?

- How Balance Transfer Cards Work

- Determining Your Balance Transfer Card Limit

- Factors Affecting Credit Limit

- Benefits of Balance Transfer Cards

- Risks of Balance Transfer Cards

- How to Maximize Your Balance Transfer

- Conclusion

What is a Balance Transfer Card?

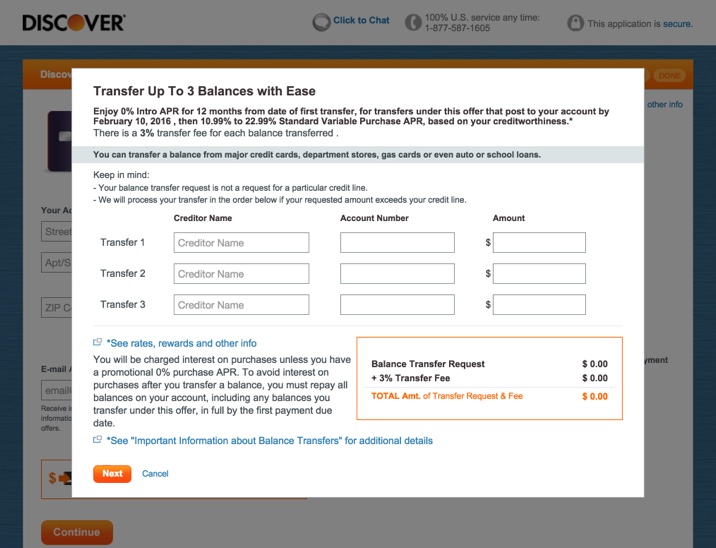

A balance transfer card is a type of credit card that allows you to transfer existing credit card debt from one or more cards to a new card. This is typically done to take advantage of lower interest rates and promotional offers that many credit card companies provide. By transferring your balance, you can reduce the amount of interest you pay over time, making it easier to pay off your debt.

How Balance Transfer Cards Work

When you apply for a balance transfer card, the issuer will review your credit history and financial situation to determine your credit limit. If approved, you can transfer your existing balances to the new card, usually within a specified promotional period where the interest rate is significantly lower, or even 0% for a limited time.

Steps to Use a Balance Transfer Card

- Research and choose the right balance transfer card based on fees and introductory rates.

- Apply for the card and wait for approval.

- Once approved, initiate the balance transfer from your old card(s) to your new card.

- Make payments on time to avoid higher interest rates after the promotional period ends.

Determining Your Balance Transfer Card Limit

The balance transfer card limit is the maximum amount you can transfer to your new card. This limit is influenced by various factors, including your credit score, income, and existing debt levels. Understanding how these factors affect your limit can help you manage your financial strategy better.

Factors Affecting Credit Limit

Several key factors influence the balance transfer card limit you may receive:

- Credit Score: A higher credit score typically leads to a higher credit limit.

- Income: Your reported income can affect the amount of credit a lender is willing to extend.

- Debt-to-Income Ratio: Lenders assess your ability to manage additional debt based on your existing debt obligations.

- Payment History: A strong payment history can positively influence your credit limit.

Benefits of Balance Transfer Cards

Using a balance transfer card comes with several benefits:

- Lower Interest Rates: Many balance transfer cards offer introductory rates as low as 0%, helping you save on interest payments.

- Debt Consolidation: You can consolidate multiple debts into a single payment, simplifying your financial management.

- Improved Credit Score: Reducing your credit utilization ratio by transferring balances can help improve your credit score over time.

Risks of Balance Transfer Cards

While balance transfer cards offer numerous advantages, they also come with potential risks:

- High Fees: Some cards may charge balance transfer fees, which can offset the savings from lower interest rates.

- Promotional Periods: If you do not pay off your balance before the promotional period ends, you may face higher interest rates.

- Impact on Credit Score: Applying for a new credit card can temporarily lower your credit score.

How to Maximize Your Balance Transfer

To make the most of your balance transfer card, consider the following tips:

- Choose a card with a long promotional period and low fees.

- Create a repayment plan to ensure you pay off your balance before the promotional rate expires.

- Avoid making new charges on your balance transfer card to prevent accumulating more debt.

Conclusion

In conclusion, understanding the balance transfer card limit is crucial for effective financial management. By utilizing balance transfer cards wisely and being aware of their limits, you can take significant steps toward reducing debt and improving your financial health. If you found this information helpful, consider leaving a comment or sharing this article with others who may benefit from it. Explore our site for more informative articles on personal finance and credit management.

Thank you for reading! We look forward to seeing you back on our site for more valuable insights.

You Might Also Like

Keanu Reeves: The Enigmatic Star And His Journey In The Film IndustryNiga Cantante: The Rising Star Of Latin Music

Dermaplaning At Home Steps: A Complete Guide For Glowing Skin

How To Dermaplane At Home: A Comprehensive Guide

Curly Hairstyle For Prom: The Ultimate Guide To Elevate Your Look

Article Recommendations

- Whitney Houston Brother Michael Died

- Samantha Sloyan Partner

- Desmond Doss

- Folake Olowofoyeku Relationships

- Archie And Lilibet Photos 2024

- Desmond Doss

- Adrianne Padalecki

- Kyle Baugher

- Candidteensnet

- Daisy Melanin Origin

:max_bytes(150000):strip_icc()/discover-it-balance-transfer_FINAL-7a6829810f7349a189279212b9e7935d.png)